Commentary: Big Tent Ideas

JOHN DIAMOND: Reject The Reckless Uniparty Tax Bill

IRS building (By Shashi Bellamkonda - Flickr: Washington DC national Mall, CC BY 2.0, https://commons.wikimedia.org/w/index.php?curid=12633433)

The House recently passed The Tax Relief for American Families and Workers Act of 2024 with significant bipartisan support. The bill provides temporary tax relief to businesses and families with children and claims to do this in a fiscally responsible manner. Unfortunately, that is not the case. It’s more reckless tax giveaways for the next two years while putting off dealing with the consequences and fiscal reform until later. This must stop.

This approach highlights several problems with current tax policy, such as the propensity for Congress to pass temporary tax provisions, spend through the tax code, and run large annual deficits. At a time when inflation is running hot and deficits are ballooning, this legislation would increase near-term fiscal stimulus and require higher taxes in the long term.

The bill reduces business taxes by allowing immediate write-offs for research and development, increasing interest expense deductions, allowing 100 percent bonus depreciation, and increasing expensing for short-lived investments. Allowing businesses to expense investments and write off the costs for research and development would boost economic growth by encouraging investment and innovation. However, giving businesses tax benefits for past investments and research expenditures will reduce economic growth. Given the historic level of debt, policymakers must refrain from giving inefficient government handouts to businesses.

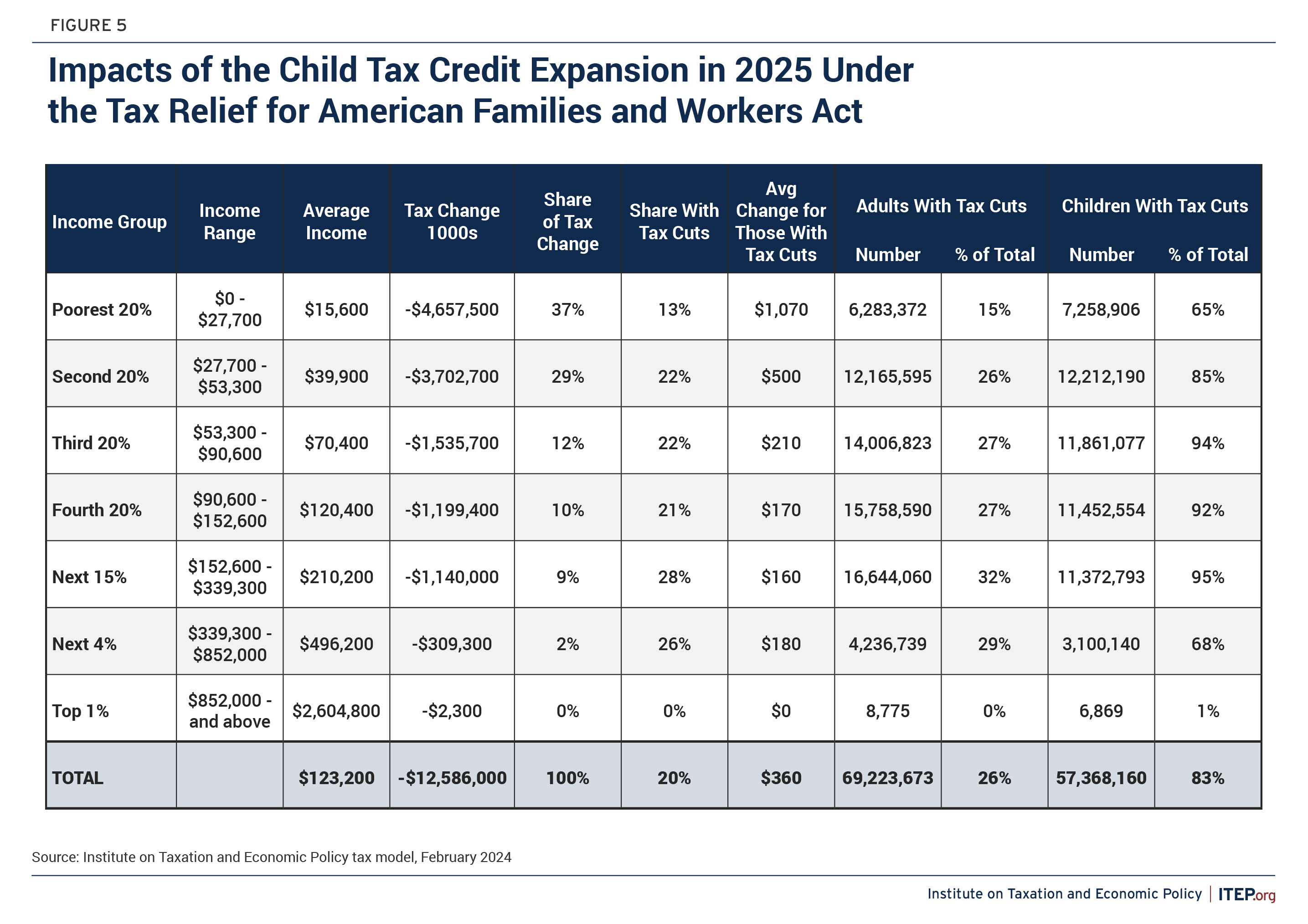

In addition, the bill would increase the child tax credit for families with children by making several changes to the tax code, such as increasing the maximum refundable credit, adjusting maximum credit values for the number of children, and indexing the credit for inflation. These policies would provide a financial benefit to low-income families with children. Nevertheless, its overall impact on reducing the adverse effects of poverty would be limited, as about one-thirdof the benefits accrue to households in the top three income quintiles. Policymakers should target help to those most in need and avoid fiscally irresponsible policies that are not well-targeted.

{kind=link}

Another problematic issue with the bill is the timing of the deficits it creates. In particular, the bill would increase deficits by roughly $150 billion in the first two years. As the Fed is battling persistent inflation, the additional fiscal stimulus would stimulate the economy at the wrong time. Suppose the Fed responds by holding the Fed’s fund rate higher for longer or increasing the rate to offset fiscal stimulus. In that case, the economy will likely slow down. Given that excess fiscal stimulus played a role in creating the current inflationary environment, it is fiscally irresponsible for Congress to add more short-term stimulus to the economy.

As noted, the bill is revenue-neutral according to estimates provided by the Joint Committee on Taxation. The bill raises revenue by disallowing claims for the Employee Retention Credit (ERC), a poorly designed pandemic-era tax policy, after Jan. 31, 2024. Using this provision as a fiscal offset is disconcerting for several reasons. First, the ERC reduced revenues by more than five times the original estimate. Second, the provision was such a mess that the IRS implemented a moratorium on new filings in September 2023. In testimony before the House Ways and Means Committee, IRS commissioner Werfel stated that the “IRS has been flooded with ERC claims, and we are concerned that many of these claims are not being filed by businesses that qualify.” While the ERC should end as early as possible, the savings must not fund temporary government handouts. Congress must exercise more fiscal discipline. If the proposed policies are genuinely desirable, they should be part of a well-designed fiscal reform.

Since much of the individual tax code sunsets at the end of 2025, tax reform will be a significant issue in the next Congress. The cost of extending the provisions set to expire is estimated to be about $3.4 trillion, but this cost increases substantially if the provisions above are extended beyond 2025. Policymakers must find the will to practice fiscal discipline. They should start by rejecting the urge to increase government handouts and instead focus on fiscally responsible tax and spending reform.

John W. Diamond is the Kelly Fellow in Public Finance and director of the Center for Public Finance at Rice University’s Baker Institute.

The views and opinions expressed in this commentary are those of the author and do not reflect the official position of the Daily Caller News Foundation.

All content created by the Daily Caller News Foundation, an independent and nonpartisan newswire service, is available without charge to any legitimate news publisher that can provide a large audience. All republished articles must include our logo, our reporter’s byline and their DCNF affiliation. For any questions about our guidelines or partnering with us, please contact [email protected].